Below is supplemental sequel to my earlier subject blogpost (https://mksudarshans.blog/2026/05/30/the-fig-leaf-of-sovereign-guarantee-tamil-nadus-temple-fund-dilemma-and-a-path-to-justice/).

It addresses the critical question:

What do we do with surplus temple funds? Temple funds must be invested, not hoarded. But the government’s solution—coercing investment in state NBFCs—is wrong. Multiple safe alternatives exist, and trustees—not the government—must decide.”

M.K.Sudarshan

(Temple Worshipper, Author, Historian, Observer-Commentator on Hindu Religious and Temple affairs, Chartered Accountant)

The Moot Question: Invest or Hoard?

The Tamil Nadu government raises a valid point when it asks:

“What do you do with surplus temple funds? Keep them under lock and key till currency notes decay, or invest them?”

This is a genuine fiduciary dilemma. Temple trustees have a duty to invest surplus funds to preserve their real value (inflation-adjusted), not just nominal value.

✓ CORRECT: Temple funds must be invested to preserve real value

✗ WRONG: Government can coerce specific investments and override trustee autonomy

This supplemental sequel addresses the critical question: If temple funds must be invested, what are the appropriate investment options?

The Government’s Solution: Invest in State NBFCs

The government’s answer is:

“Invest in TNPFIDC and TNTDFC.”

But this answer is legally flawed for three reasons:

1. Not the ONLY Investment Option

Surplus temple funds can be invested in multiple safe alternatives. The government offers ONE option when MULTIPLE safe alternatives exist:

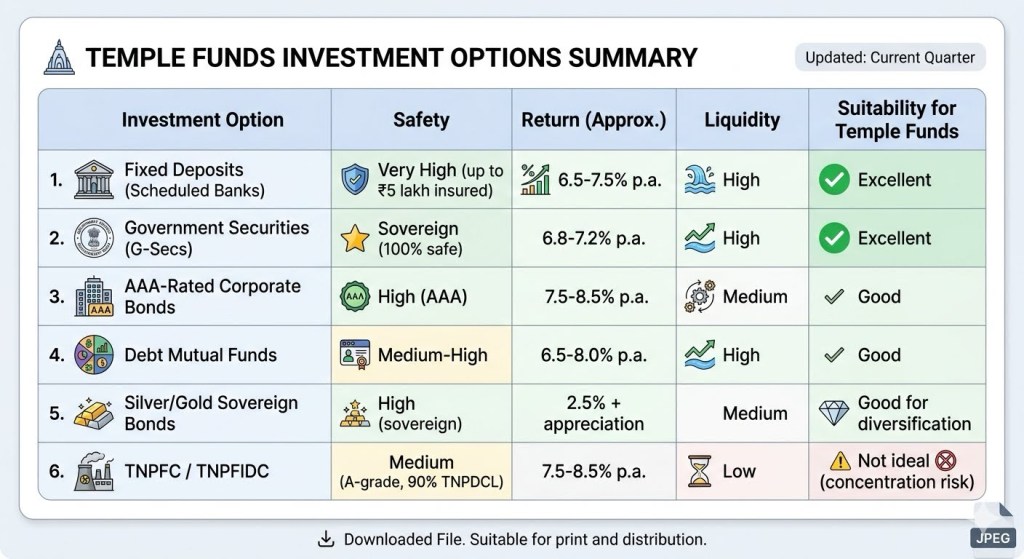

Table 1: Safe Investment Options for Temple Funds

Key Finding: Banks, G-secs, and AAA bonds offer comparable or better safety with no concentration risk.

2. Concentration Risk Violates Fiduciary Duty

The Prudent Investor Rule (common law standard for trustees) requires trustees to follow specific investment principles. Here’s how TNPFIDC measures up:

Table 2: Prudent Investor Rule Requirements vs. TNPFIDC

Bottom Line: A prudent trustee operating under fiduciary duty would NOT invest 90%+ of temple funds in a single NBFC with extreme concentration risk.

3. The Sovereign Guarantee is a Fig Leaf

The government argues:

“We offer sovereign guarantee, so funds are safe.”

But this is circular:

- Government guarantees TNPFIDC deposits

- TNPFIDC lends 90% to TNPDCL (TANGEDCO)

- TNPDCL is debt-ridden (₹1.62 lakh crore losses)

- If TNPDCL defaults, government must bail it out

- Government guarantees itself — no real protection

This is like guaranteeing your own credit card bill — it doesn’t make you creditworthy.

The sovereign guarantee provides legal protection (if TNPFIDC defaults, state pays), but it does NOT eliminate:

- Concentration risk – 90% in single borrower

- Credit risk – A-grade rating (not AAA)

- Liquidity risk – Long-term lock-in

- Fiduciary breach – Trustees didn’t choose

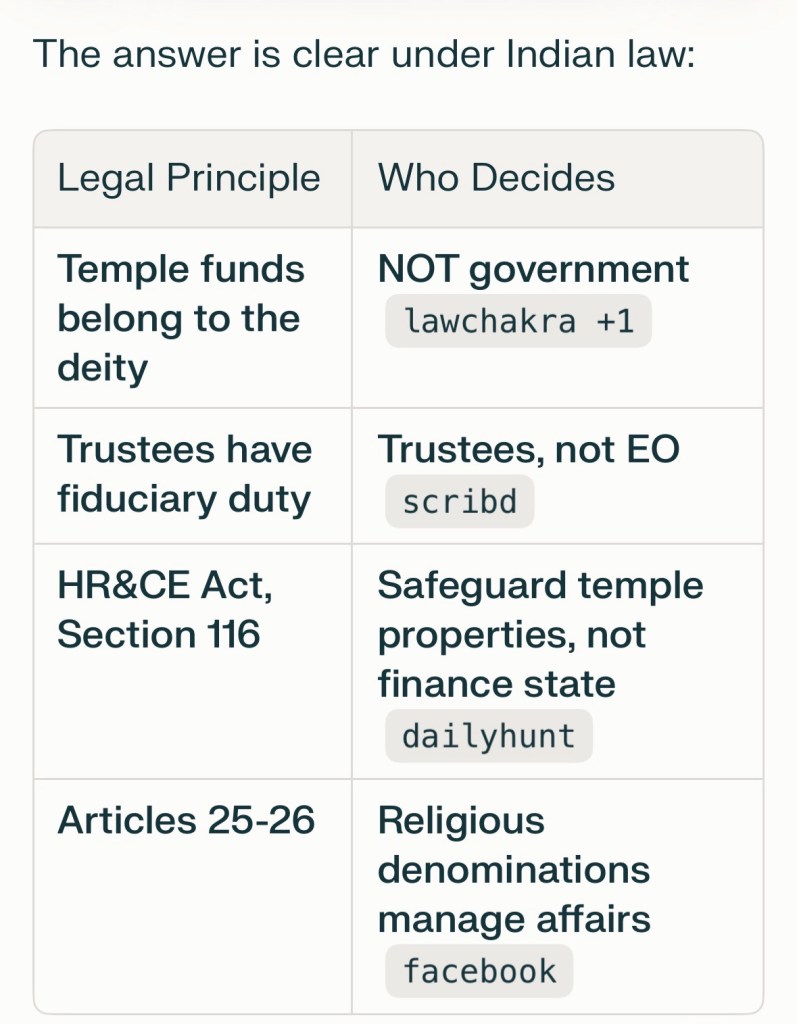

The Real Question: Who Decides?

The government’s argument hides a fundamental question:

Who has the right to decide how temple funds are invested?”

The answer is clear under Indian law:

Table 3: Who Decides Temple Fund Investments?

The government is not the owner of temple funds. It is merely the administrator (when trustees don’t exist). As administrator, it has a fiduciary duty to act in the deity’s interest, NOT the state’s interest.

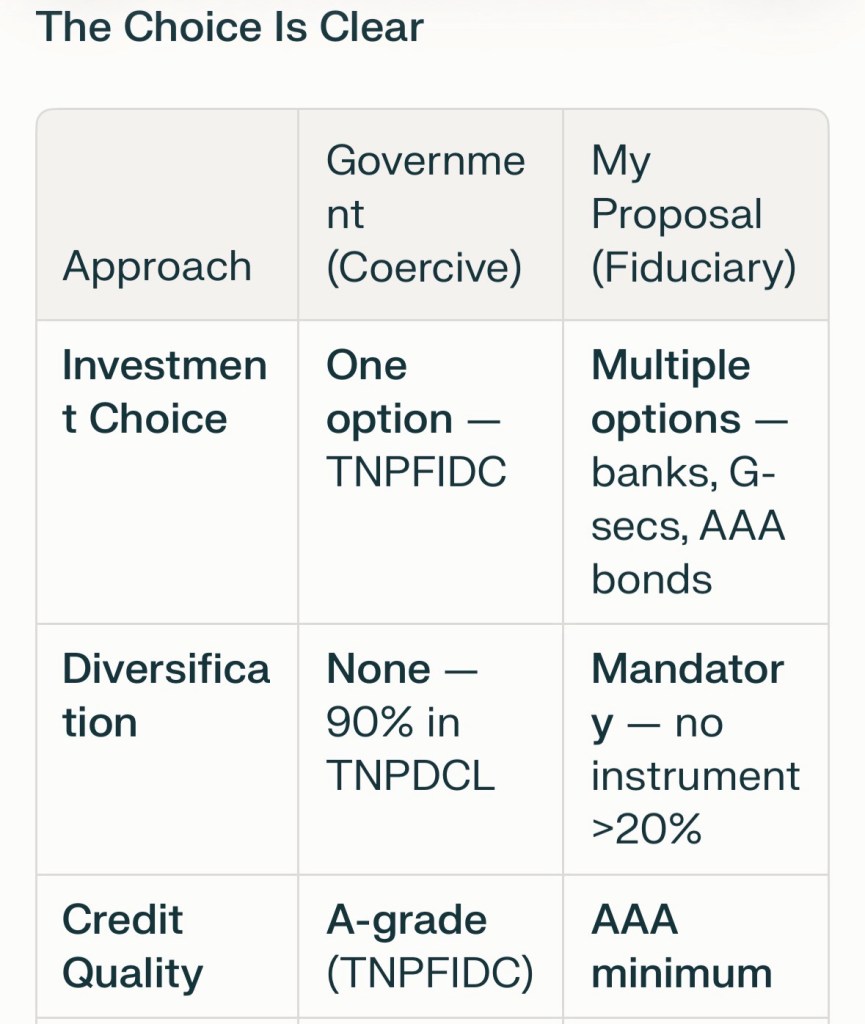

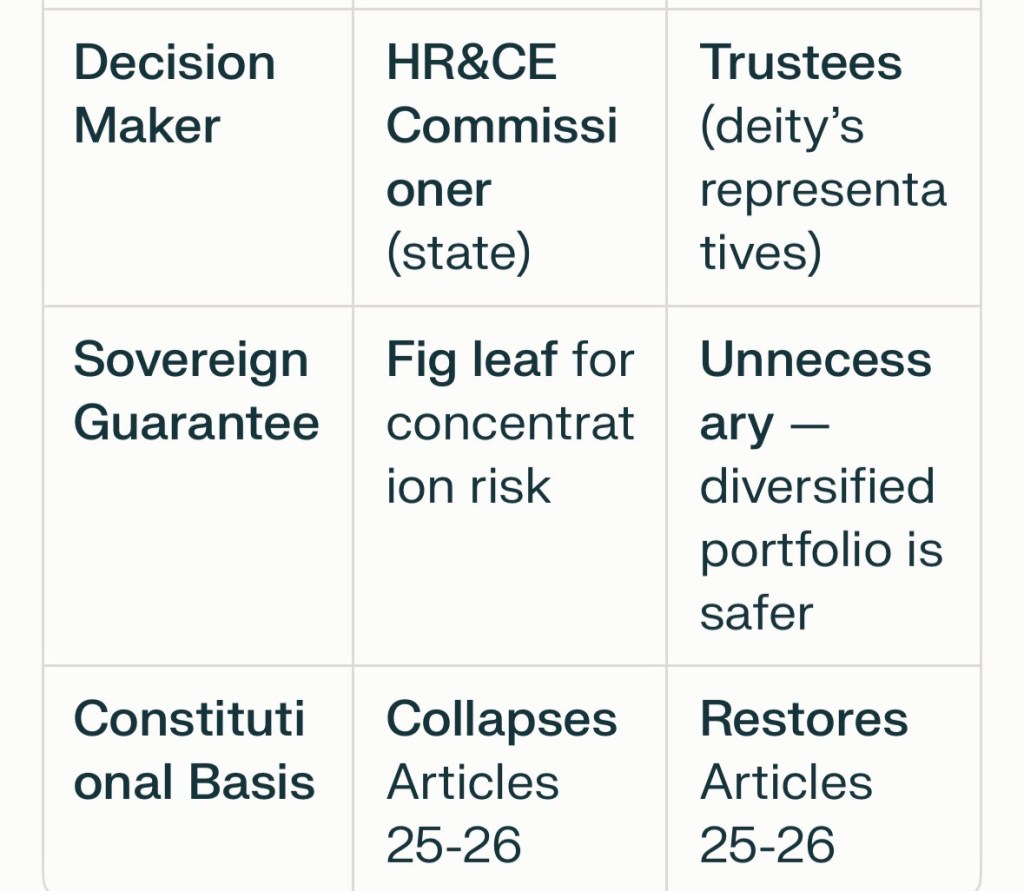

My Proposed Solution: Prudent Investment Framework

Instead of coercing temples into TNPFIDC, the government should adopt a prudent investment framework that respects trustee autonomy while ensuring safe investment:

Table 4: Government’s Approach vs. Fiduciary Standard

This would protect temple funds while respecting trustee autonomy and fiduciary duty.

The Choice Is Clear

The government’s argument that “funds must be invested” is TRUE, but their solution is WRONG:

Government Claim Vs Reality

✓ TRUE: Temple funds must be invested to preserve real value

✗ WRONG: Government can coerce specific investments

✓ TRUE: Sovereign guarantee provides some protection

✗ WRONG: Guarantee eliminates concentration risk

✓ TRUE: Investment is necessary

✗ WRONG: TNPFIDC is the only option

✓ TRUE: Surplus funds cannot sit idle

✗ WRONG: HR&CE Commissioner should decide for trustees

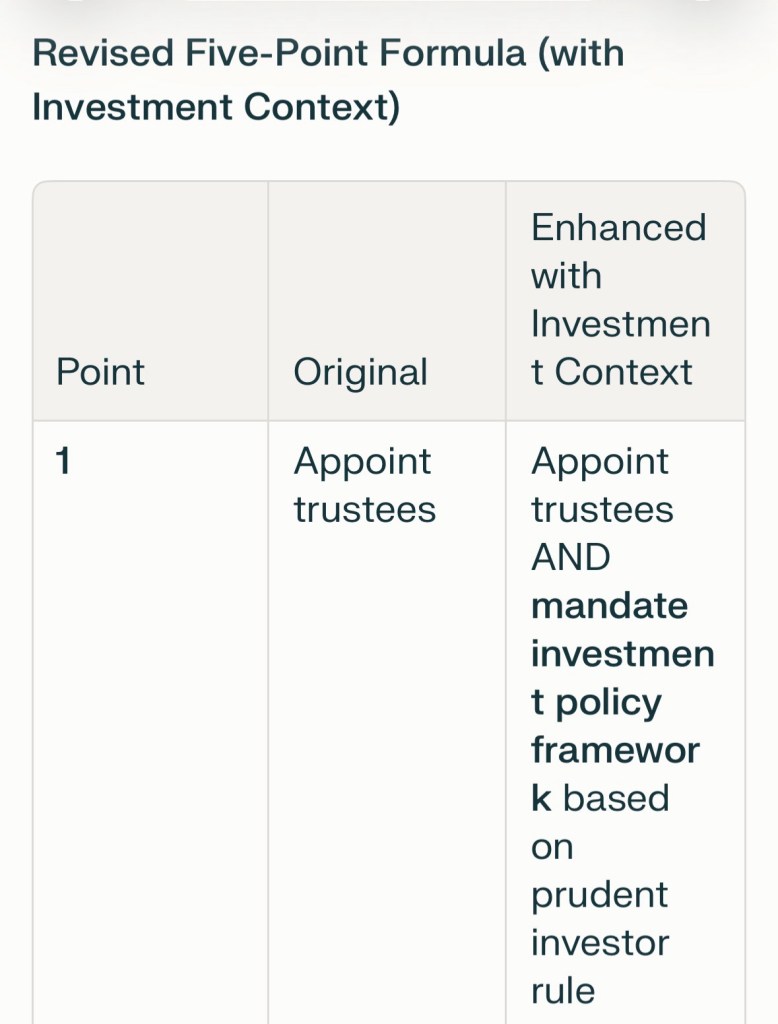

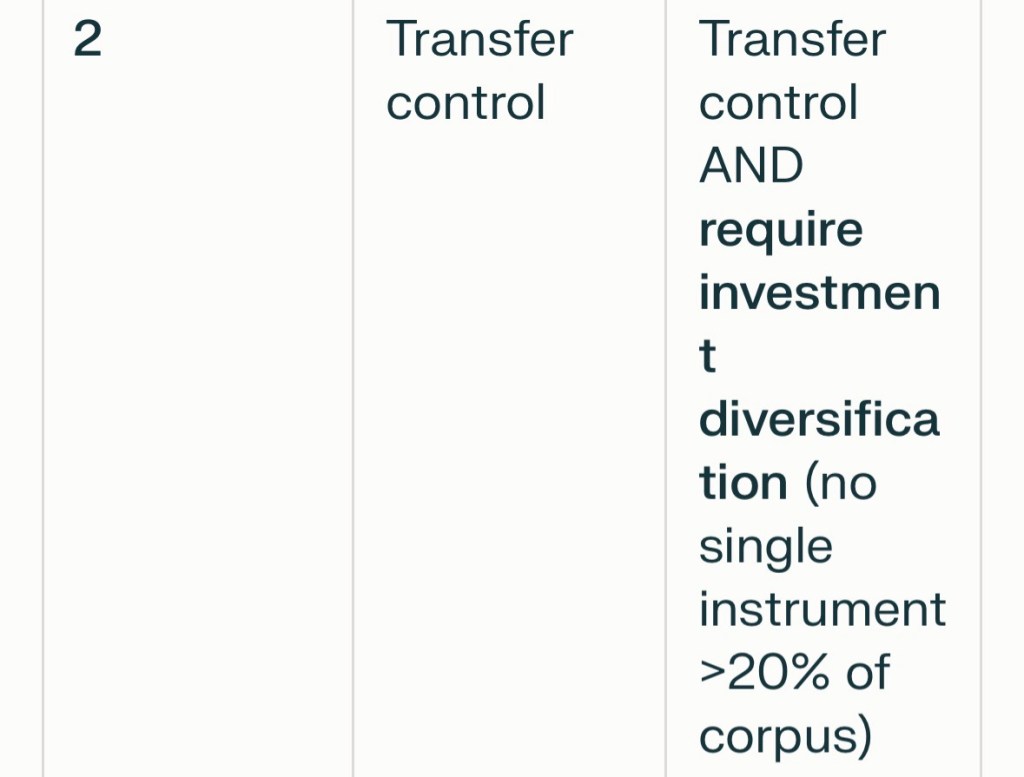

How This Strengthens the Five-Point Formula

The five-point due process formula that I had proposed (see my previous blogpost) is even more justified when we consider the fiduciary duty to invest:

Table 5: Five-Point Formula Enhanced with Investment Context

The formula ensures:

- Trustees are appointed (Point 1)

- Trustees have control (Point 2)

- Trustees decide investment (Point 3)

- Funds are protected during decision (Point 4)

- PIL is resolved based on trustee decisions (Point 5)

Conclusion: Investment is Necessary, Coercion is Not

The Tamil Nadu government’s argument that “temple funds must be invested” is absolutely correct. But their solution—coercing investment in TNPFIDC—is legally and fiscally flawed.

The Path Forward:

- Trustees must be appointed for all 31,000 temples

- Trustees must decide on investment options (not government)

- Multiple safe alternatives exist — banks, G-secs, AAA bonds

- Diversification is mandatory — no concentration risk

- Fiduciary duty must be fulfilled — deity’s interest, not state’s

The sovereign guarantee is a fig leaf that doesn’t address the core issue: trustees must decide, not the government.

This supplemental sequel here strengthens my original op-ed by showing that investment is necessary, but coercion is wrong. The five-point formula ensures both: investment happens (through trustees) and coercion is removed (through trustee autonomy).

References

- Rating Rationale: TNPFIDC — Brickwork Rating (September 9, 2025)

- HC questioned ₹2,700cr in TNPFIDC lending 90% to debt-ridden TNPDCL — Times of India (May 27, 2026)

- Tamil Nadu’s outstanding debt to touch ₹10.71 lakh crore in 2026-27 — Investment Guru India (February 16, 2026)

- Madras HC: “Temple Funds Belong To Deity, Can’t Be Used For Government Projects” — Law Chakra (August 27, 2025)

- Madras High Court questions Tamil Nadu’s move to deposit temple funds in state NBFCS — MyInd (May 21, 2026)

- Appointment of trustees for temples by May ’24, HC told — Times of India (2023)

- SC asks TN to list steps for appointment of trustee committee for temples — Business Standard (December 10, 2024)

: #templefunds #HRCE #TNPFIDC #fiduciaryduty #templeinvestment #MadrasHighCourt #PIL #TamilNadu #ConstitutionalLaw #prudentinvestor

One thought on ““What Do We Do With Surplus Temple Funds?”- The Fig Leaf of Sovereign Guarantee: (A Supplementary post)”